To help you complete your tax return, especially if you’ve been working from home, this checklist outlines income and expenses you need to disclose to the Australian Taxation Office (ATO) when lodging your return. We’ve also provided an overview of the types of tax offsets and deductions you may be entitled to claim, plus other handy tax tips.

Income

- Gross salary, wages, earnings, allowances, benefits, tips, and directors’ fees as per the pay as you go (PAYG) payment summary supplied by your employer.

- Lump sum and termination payments as per the PAYG payment summary supplied by your employer.

- Annuities or other pensions, such as accountbased pensions, as per PAYG payment summary or statements provided by your financial institution or super fund.

- Taxable Government allowances or pensions, such as the JobSeeker Payment, Youth Allowance and Age Pension.

- Interest earned as per your bank, mutual bank or credit union statements.

- Dividends received or reinvested, including any franking credits attached as per the dividend statements provided by the company.

- Distributions from partnerships and trusts, including managed funds, as per the distribution statement provided by the partnership or trust.

- Details of any capital gains or losses incurred from the sale of (or other dealings involving) capital gains tax (CGT) assets, such as shares and property. This includes dates and values of acquisitions and disposals, as per purchase and sale documents.

- Rent received from investment properties as per real estate agent statements or personal records.

- Details of any foreign source income (including overseas pensions) earned or received, foreign assets held, and any foreign taxes paid.

Expenses

- Work-related expenses that have not been reimbursed by your employer.

- Deductible work from home (WFH) expenses during the Coronavirus crisis not reimbursed by your employer. For more information, please see page 2.

- Motor vehicle expense details for work-related travel in a personal vehicle, including the workrelated kilometres travelled. This excludes travel to and from work.

- Other work-related travel expenses, such as taxis, public transport, and bridge tolls.

- Purchase of compulsory uniforms, protective clothing, and laundry costs for work-related purposes.

- Self-education expenses, including fees, books, stationery, travel, and parking.

- Union fees and memberships to industry and professional organisations.

- Purchase of sun protection, hats, sunglasses, and sunscreen if you need sun protection at work.

- Purchase of tools of trade or equipment for workrelated purposes.

- Telephone accounts for work-related calls.

- If you are paid an overtime meal allowance under an award, you can claim up to the reasonable allowance expense amount set out by the ATO.

- Attendance fees and travel for work-related seminars, conferences, and conventions. Books, journals, subscriptions, and your professional library expenses.

- Home office set-up expenses such as depreciation on purchase of equipment, including computers, telephones, and furniture. Details of home office running expenses such as heating, cooling, lighting, and cleaning.

Investment-related expenses

- Telephone accounts for investment-related calls.

- Attendance fees and travel for investment seminars, conferences, and conventions.

- Interest paid and fees charged on money borrowed for investments, such as shares.

- Bank fees incurred on investment-related activities and accounts.

- Property rental expenses, including advertising, council and water rates, insurance, interest on loans, real estate management fees, repairs and maintenance, lease preparation, and depreciation and capital works (such as buildings and structural improvements) deductions.

- Please note, from 1 July 2017, travel expenses relating to inspecting, maintaining, or collecting rent for a residential rental property cannot be claimed as a deduction.

General expenses

- Donations of $2 or more to registered charities.

- Tax preparation fees, including travel to your tax agent.

Tax offsets and deductions

You may be entitled to the following tax offsets (rebates) and deductions for the year ended 30 June 2022.

Deductions for expenses related to working from home due to COVID

If you are working from home due to the COVID crisis and incur expenses that are not reimbursed by your employer, you may be able to claim them as a tax deduction. The expenses must be directly related to working from home and you need to keep a record of your working from home hours and your expenses. There are three ways you can choose to calculate additional running expenses: Shortcut method – A deduction of $0.80 for each hour worked from home due to COVID is allowed if you incur additional deductible running expenses due to working from home.

Fixed-rate method – allows: • a rate of $0.52 per hour for the cost of utilities, cleaning, and depreciation of office furniture • work-related phone and internet expenses, computer consumables, and stationery • work-related depreciation of a computer, laptop, or similar device.

Actual cost method – claim the actual work-related portion of all running expenses, calculated on a reasonable basis.

Private health insurance offset

Depending on your income and age, you may be eligible for a tax offset of up to 33.4% on your health insurance. If you haven’t claimed a reduced premium from your health fund, then you can claim an offset in your tax return.

Spouse super contribution offset

If you made personal superannuation contributions on behalf of a spouse, there is a tax offset of up to $540 per year. This is available for spouse contributions of up to $3,000 per year, where your spouse earns less than $37,000 per year, and a partial tax offset for spousal income up to $40,000 per year.

Super related tax offsets | Australian Taxation Office (ato.gov.au)

Senior Australian’s pensioner tax offset

If you are eligible for the senior Australians pensioner tax offset (SAPTO) you are able to earn more income before you have to pay tax and the Medicare levy. Super tax hints Super is a very tax-effective way to save for retirement. The following section contains some tips to help you maximise your super.

Super tax hints

Super is a very tax-effective way to save for retirement. The following section contains some tips to help you maximise your super.

Contribution limits

For the 2021/22 financial year the maximum nonconcessional (or after-tax) super contributions are capped at $110,000 per person per year or up to $330,000 over three years using the bring-forward provisions. The ability to make non-concessional contributions and take advantage of the three-year bring forward provision is subject to your total super balance at 30 June the previous financial year, your age and whether you have satisfied the work test (if between ages 67–74).

Concessional contributions, or those made with pre-tax money, are limited to $27,500 per person per year. Unused concessional contribution caps from the 2018/19 financial year and later years may be used for up to five financial years as long as the member’s total superannuation balance on 30 June prior to the financial year of contribution is less than $500,000.

Please note, voluntary concessional contributions, such as salary sacrifice or personal deductible contributions, are subject to age restrictions and the work test and work test exemption (if between ages 67–74).

Salary sacrifice

A salary sacrifices strategy allows you to make contributions to super from your pre-tax salary. Your salary is then reduced by the amount you choose to sacrifice. The benefits of this are two-fold: not only does your super balance increase, but this strategy could also reduce your taxable income and therefore the amount of tax you pay. Also, super contributions are concessionally taxed at just 15% (up to 30% for individuals with income over $250,000) instead of your marginal tax rate, which could be as high as 47% (including 2% Medicare levy).

Personal deductible contributions

Since 1 July 2017, if you are eligible to contribute to super, you may make voluntary personal contributions and claim a tax deduction up to your concessional contribution cap. This gives you greater flexibility to top up your concessional contributions made by your employer, especially if your employer does not offer salary sacrifice. For example, you can time your final contributions leading up to 30 June each year and make the most of your concessional contribution limits and the resulting tax benefits.

Super co-contributions

If you receive at least 10% of your income from employment or self-employment and you earn less than $41,112, you may be eligible for the maximum super co-contribution of $500 from the Government for an after-tax contribution to super of $1,000. The co-contribution phases out once you earn $56,112 or more. The ATO uses information on your income tax return and contribution information from your super fund to determine your eligibility.

Super co-contributions | Australian Taxation Office (ato.gov.au)

Super splitting

If you want to split your super contributions with your spouse, don’t forget this usually can only be done in the year after the contributions were made. Therefore, from 1 July 2021, you may be able to split up to 85% of any concessional (or pre-tax) contributions you made during the 2020/21 financial year with your spouse. Apart from making the most of your super, there are other ways you can minimise your tax liability.

Capital gains and losses

A capital gain arising from the sale of an investment property or shares and capital losses can be used to offset the capital gains. For example, you may have sold investments that were no longer appropriate for your circumstances and any capital losses realised as a result can be offset against any capital gains you have realized throughout the year. Unused losses can be carried forward to offset capital gains in future years. Financial advice should be sought before making changes to your investments.

Prepaying interest

If you have an investment loan you can arrange to prepay the interest on that loan for up to 12 months and claim a tax deduction in the same year the interest was prepaid.

Negative gearing

Negative gearing is another strategy used to manage tax liabilities. Geared investments use borrowed funds to enable a higher level of investment than would otherwise be possible. Negative gearing refers to the cost of borrowing exceeding the income generated by the investment. This excess cost can reduce the tax you pay on other income. If you invest in shares, you may obtain imputation credits which can be used to further reduce the amount of tax you pay.

Income protection insurance

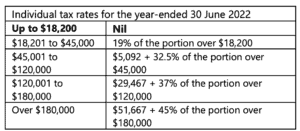

If you hold an income protection policy in your name, then any premium payments you make are tax deductible. Resident tax rates for 2021/22 Note: Medicare levy of 2% will also apply where applicable.

For further information, please contact your financial adviser.

The purpose of this website is to provide general information only and the contents of this website do not purport to provide personal financial advice. Denaro Wealth strongly recommends that investors consult a financial adviser prior to making any investment decision. The contents of the Denaro Wealth website does not take into account the investment objectives, financial situation or particular needs of any person and should not be used as the basis for making any financial or other decisions. The information is selective and may not be complete or accurate for your particular purposes and should not be construed as a recommendation to invest in any particular product, investment or security. The information provided on this website is given in good faith and is believed to be accurate at the time of compilation.